While it’s a topic many would like to avoid talking about, dealing with life expectancy is vitally important when mapping out your retirement plan. Any retirement plan that doesn’t make certain assumptions about when clients are “expected” to pass away isn’t very good.

What’s the best way to calculate your Life Expectancy (LE)?

There are three simple ways to calculate your LE:

1) Use the CDC (Center for Disease Control) LE tables

2) Use the IRS (Internal Revenue Service) RMD (Required Minimum Distribution) LE table

3) Use an LE table provided by a life insurance company

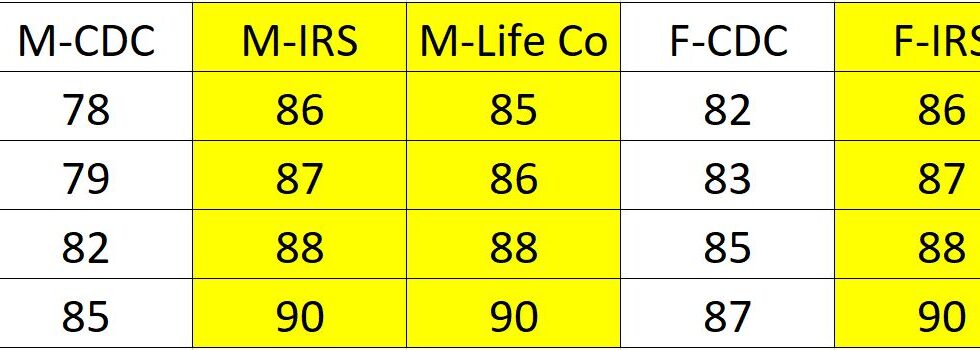

Which one should be used? It seems that most people use the CDC table. This could be a mistake. Why? Because it is significantly different than the IRS and life insurance company’s numbers. See the following chart with LE numbers for various ages.

Why should we trust the life insurance company’s number? Because they have been running these numbers for over 100 years. They know how to price life insurance so they make a profit.

Generally speaking, few “trust” the IRS but since their numbers are so similar to the insurance companies’ numbers, it lends credibility to the numbers.

What if you are healthy?

Neither the IRS nor CDC take into account health. The insurance company numbers from above assume you are rated “standard” for underwriting purposes. What if you are rated “preferred”?

45-year old = 90

55-year old = 91

65-year old = 92

75-year old = 94

Being healthy extended the life expectancy numbers by two years.

What if you are married? The joint life numbers are very interesting. Let’s look at the life insurance numbers for both “standard” and “preferred” underwriting.

Standard

45-year old = 92

55-year old = 92

65-year old = 93

75-year old = 94

Preferred

45-year old = 95

55-year old = 95

65-year old = 95

75-year old = 97

Why do these numbers matter?

Simply stated, it’s impossible to put together a safe and secure retirement plan if you are not using the right LE tables to best plan for when you are going to pass away.

If you use the CDC guidelines and you are 55-years old, you’ll plan on living until age 79.

If you use the life insurance company numbers, you’d plan on living until age 86.

If you are healthy, and used the life insurance company numbers, you’d plan on age 91.

If you are married and are both healthy, you’d plan on the 2nd spouse passing away at age 95.

There are significant financial/retirement planning decisions that will be dramatically different if you are planning to live to age 79 vs. 86 vs. 95.

Guaranteed income for life products*

Many people and even many advisors are unaware of the fact that there are guaranteed income for life products available. They are polarizing products in that some advisors think they should never be used and others who think they should always be used.

The reality is that these products can be useful tools for clients who want certainty in their retirement plan.

Want help mapping out your future retirement plan?

If you’d like help putting together a comprehensive retirement plan (one that takes into account your proper life expectancy and one that will use the available tools to help you generate retirement income while protecting your assets), please feel free to reach out using the contact information below.

* Any reference to Guaranteed income for life products are backed by the financial strength and claims paying ability of the issuing insurance company and may be subject to caps, restrictions, fees and surrender charges as described in the annuity contract.